Want the Max $5,181 Social Security Benefit in 2026? Here’s What It Takes

Social Security plays a vital role in retirement planning for millions of Americans. While most retirees receive a modest monthly benefit, a very small group qualifies for the maximum possible Social Security payment. In 2026, that top amount is $5,181 per month — but reaching it requires specific income levels, long-term consistency, and careful timing.

Here’s a clear breakdown of what it takes to receive the highest Social Security benefit available.

What Is the Maximum Social Security Benefit in 2026?

The highest possible monthly Social Security retirement benefit in 2026 is $5,181, but this amount is only available to retirees who meet strict eligibility criteria.

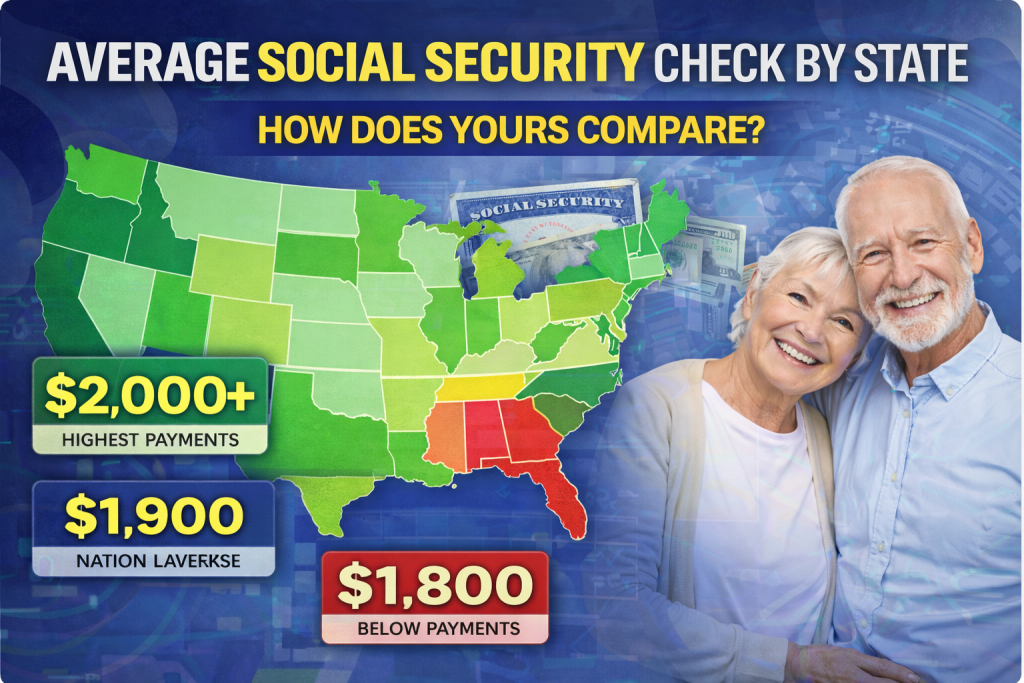

For comparison, the average Social Security retirement benefit after cost-of-living adjustments is just over $2,000 per month, meaning the maximum benefit is more than double what most retirees receive.

Step 1: Earn the Maximum Taxable Income for Many Years

Social Security calculates your benefit using your 35 highest-earning years. If you work fewer than 35 years, zero-income years are included, lowering your average.

Each year, there is a maximum taxable earnings limit, which is the highest amount of income that counts toward Social Security. In 2026, that limit is $184,500.

To qualify for the maximum benefit:

-

You must earn at or above the taxable income limit in most or all of your top 35 earning years.

-

Income above the limit does not increase benefits further.

-

Missing high-earning years can significantly reduce your final benefit amount.

This requirement alone makes the maximum benefit unreachable for most workers.

Step 2: Delay Claiming Benefits Until Age 70

Even with a perfect earnings record, when you claim Social Security matters.

-

Claiming at age 62 permanently reduces your benefit.

-

Claiming at full retirement age provides your standard benefit.

-

Delaying until age 70 earns delayed retirement credits, increasing benefits by roughly 8% per year after full retirement age.

To receive the full $5,181 per month, you must wait until age 70 to start collecting benefits.

How Rare Is the Maximum Benefit?

Very few retirees qualify for the maximum Social Security payment. Achieving it requires:

-

Consistently high income for decades

-

Minimal gaps in employment

-

Delaying retirement benefits until age 70

Because of these conditions, only a small percentage of workers ever receive the maximum benefit.

What This Means for Retirement Planning

✔ Most retirees will not receive the maximum

And that’s normal. Social Security is designed to replace only part of pre-retirement income.

✔ Timing can matter as much as earnings

Even if you don’t earn the maximum wage, delaying benefits can still significantly increase your monthly payments.

✔ Social Security should be one part of retirement income

Savings, pensions, and personal investments remain important for long-term financial security.

✔ Understanding the rules helps

Knowing how benefits are calculated allows better decisions about working longer, earning more, or delaying claims.

Bottom Line

The $5,181 maximum Social Security benefit in 2026 is achievable only for workers with exceptionally high and consistent earnings who delay claiming benefits until age 70. While most Americans will receive less, understanding these rules can still help maximize your personal benefit and improve retirement outcomes.

Social Security remains a critical foundation of retirement income — but planning ahead makes all the difference.

Leave a Comment