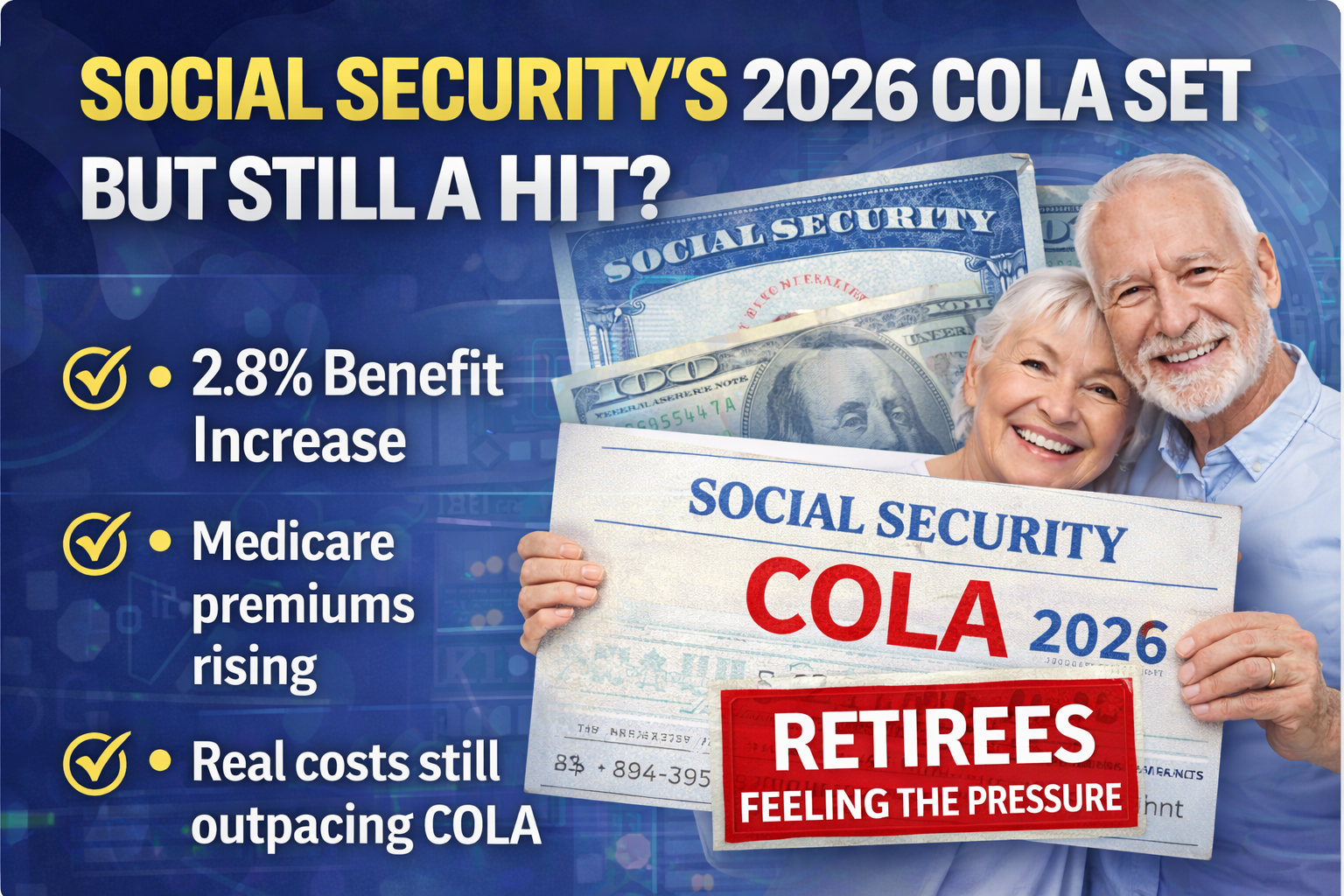

Social Security’s 2026 COLA Is Set — Why Retirees Could Still Take a Major Financial Hit

As 2026 gets underway, millions of American retirees are seeing their Social Security benefit checks rise slightly thanks to the newly confirmed Cost-of-Living Adjustment (COLA). While the boost in monthly benefits reflects ongoing inflation, many seniors are discovering that it may not provide meaningful financial relief this year.

What the COLA Means for Your Benefits in 2026

In 2026, Social Security recipients are receiving a 2.8% increase in their monthly benefits. This adjustment applies to retirement, survivor, and disability payments and begins with checks issued early in the year.

A 2.8% COLA is slightly higher than the 2.5% increase seen in 2025, but it is far below the unusually large boosts during peak inflation years earlier in the decade. For many retirees, that modest increase translates to only a small rise in monthly income.

Despite the raise, many beneficiaries feel their purchasing power is not keeping pace with real costs because prices for essentials like healthcare and housing remain high.

Why Many Retirees Still Feel Financial Pressure

1. Everyday Costs Are Still High

While inflation has eased from its peak, prices for critical goods and services — such as medical care, prescription drugs, housing, insurance, and utilities — continue to rise faster than the general inflation index used to determine COLA. Seniors typically spend a larger share of their fixed income on these essentials, so even a slight price increase can have a big impact.

2. Medicare Premiums Eat Into the COLA

One of the biggest factors reducing the real value of the 2026 COLA is the increase in Medicare Part B premiums. The standard monthly premium rose from one year to the next, meaning many seniors have that amount automatically deducted from their Social Security checks before they see it. For many retirees, this increase absorbs a significant portion of the 2.8% benefit raise.

The net result is that some retirees may feel they are no better off today than before the COLA was applied, especially once healthcare costs are factored in.

3. COLA Doesn’t Match Retiree Cost Patterns

The Social Security COLA is calculated using an inflation index based on spending patterns of urban wage earners, not retirees. Because older adults tend to spend more on items that have experienced higher inflation — like healthcare and housing — the standard COLA formula often underestimates the actual cost pressures faced by retirees.

This mismatch has contributed to a growing gap between the increase in Social Security benefits and the real cost of living for many older Americans.

What Retirees Should Expect in 2026

For 2026, the COLA provides stability rather than substantial relief. The modest increase helps ensure that benefits do not lose value completely due to inflation, but it does not restore purchasing power lost during earlier years when prices rose more dramatically.

Retirees on fixed incomes may need to adjust their planning strategies to cope with ongoing cost pressures. This could include reviewing healthcare coverage, re-evaluating household budgets, or seeking financial advice to make the most of limited resources.

Despite the challenges, Social Security remains a foundational source of income for millions of older Americans, helping cover essential expenses and providing financial security in retirement.

Key Takeaways

- 2026 COLA: Benefits rise by 2.8%, beginning in January.

- Modest Increase: The raise is larger than last year’s adjustment but still limited.

- Healthcare Costs: Rising Medicare premiums and other healthcare expenses absorb much of the benefit increase.

- Retiree Concerns: Many seniors feel that the COLA does not keep pace with actual living costs.

- Financial Planning: Careful budgeting and planning remain important for retirees relying on Social Security.

Leave a Comment