Several important Social Security tax and benefit changes take effect in 2026, affecting both workers who pay into the system and retirees who receive monthly benefits. While the changes are not dramatic, they can have a meaningful impact on paychecks, retirement income, and long-term planning.

This guide explains what is changing, who is affected, and how to plan wisely — without exaggeration or misinformation.

Overview of Key Social Security Changes in 2026

| Category | 2025 | 2026 | What It Means |

|---|---|---|---|

| Payroll tax rate (employees) | 6.2% | 6.2% | The tax rate stays the same |

| Payroll tax rate (self-employed) | 12.4% | 12.4% | No rate change |

| Maximum taxable earnings | $176,100 | $184,500 | Higher earners pay tax on more income |

| Cost-of-living adjustment (COLA) | — | +2.8% | Monthly benefits increase |

| Full retirement age | 66–67 (by birth year) | Same | No change |

| Earnings limit (before full retirement age) | Lower | Higher | More flexibility for working beneficiaries |

What’s Changing With Social Security Taxes in 2026

Payroll Tax Rate Remains the Same

The Social Security payroll tax rate does not increase in 2026:

- Employees continue to pay 6.2%

- Employers match that amount

- Self-employed individuals pay 12.4%

Maximum Taxable Earnings Increase

The maximum amount of income subject to Social Security tax rises from $176,100 to $184,500.

What this means:

- Workers earning below $176,100 see no change

- Workers earning above that level will pay tax on an additional $8,400

- High earners will contribute about $520 more in Social Security tax for the year

This adjustment helps support the long-term funding of the Social Security program and may slightly increase future benefit calculations for some workers.

What’s Changing With Social Security Benefits

Cost-of-Living Adjustment (COLA)

In 2026, Social Security recipients receive a 2.8% cost-of-living increase. This raises the average monthly benefit by roughly $50–$60, depending on the individual benefit amount.

The goal of COLA is to help benefits keep pace with inflation, though it may not fully offset rising costs for housing, healthcare, and food for some retirees.

Earnings Limits for Those Who Work While Collecting

If you claim Social Security before full retirement age and continue working:

- You can earn more in 2026 before benefits are temporarily reduced

- Higher limits apply in the year you reach full retirement age

- Once you reach full retirement age, there is no earnings limit

Any benefits withheld due to earnings are not lost permanently — they are recalculated into your benefit amount later.

Common Questions Answered

Does the Social Security tax rate increase in 2026?

No. The tax rate stays the same. Only the income cap subject to tax increases.

Will paying more Social Security tax increase my future benefits?

Possibly. Higher taxed earnings can improve your lifetime earnings record, which may slightly raise future benefits — especially if the new earnings replace lower-earning years in your calculation.

Who is affected by the higher taxable earnings limit?

Only workers earning above $176,100. Most workers earning less than that see no change.

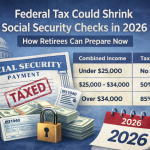

Are Social Security benefits taxed differently in 2026?

The basic rules for taxing Social Security benefits remain unchanged. However, changes in other income — such as pensions, IRA withdrawals, or wages — can affect how much of your benefit is taxable.

Practical Planning Advice for 2026

1. Review Your Earnings Record

Check your Social Security earnings history to ensure your income is correctly recorded. Errors can reduce future benefits.

2. Plan for Taxes on Benefits

If your total income exceeds certain thresholds, part of your Social Security benefits may be taxable. Managing withdrawals from retirement accounts can help reduce taxes.

3. Watch Medicare Premiums

Medicare premiums are deducted from Social Security checks for many beneficiaries. Even with a COLA increase, higher premiums can reduce the net amount you receive.

4. Consider Delaying Benefits if Possible

Delaying Social Security beyond full retirement age increases your monthly benefit up to age 70. For those who can afford to wait, this can significantly improve long-term income security.

Bottom Line

| Change | Impact |

|---|---|

| Higher taxable earnings cap | More Social Security tax for high earners |

| 2.8% COLA increase | Modest boost to monthly benefits |

| Higher earnings limits | More flexibility for working retirees |

The 2026 Social Security changes are gradual but important. Understanding how taxes, benefits, and earnings limits work together allows you to plan more confidently for retirement and avoid unexpected surprises.

Leave a Comment