Many Americans assume their Social Security benefits are tax-free. In reality, a federal tax rule can reduce the net amount you receive each month, especially if you have other income. This issue is expected to affect more retirees in 2026 as income levels rise and benefit amounts increase.

This guide explains how the tax works, who is affected, and what practical steps you can take to plan ahead.

Why Some Social Security Benefits Are Taxed

Social Security benefits may be subject to federal income tax if your total income crosses certain thresholds. The IRS uses a measure called combined income, which includes:

- Adjusted gross income (AGI)

- Tax-exempt interest

- 50% of your Social Security benefits

If this combined amount exceeds set limits, up to 50% or even 85% of your benefits may become taxable.

These income thresholds have not been adjusted for inflation for decades, meaning more retirees become taxable each year as their incomes and benefits rise.

2026 Factors That Could Increase Your Tax Burden

Several changes in 2026 may push more retirees into the taxable range:

1. Cost-of-Living Adjustment (COLA)

Benefits increased by 2.8% in 2026, which raises monthly payments but can also push total income above tax thresholds.

2. Additional Retirement Income

Withdrawals from:

- 401(k)

- IRA

- Pensions

- Part-time work

can increase combined income and make benefits taxable.

3. Fixed Tax Thresholds

Because the tax limits remain unchanged, even modest income growth can trigger taxation.

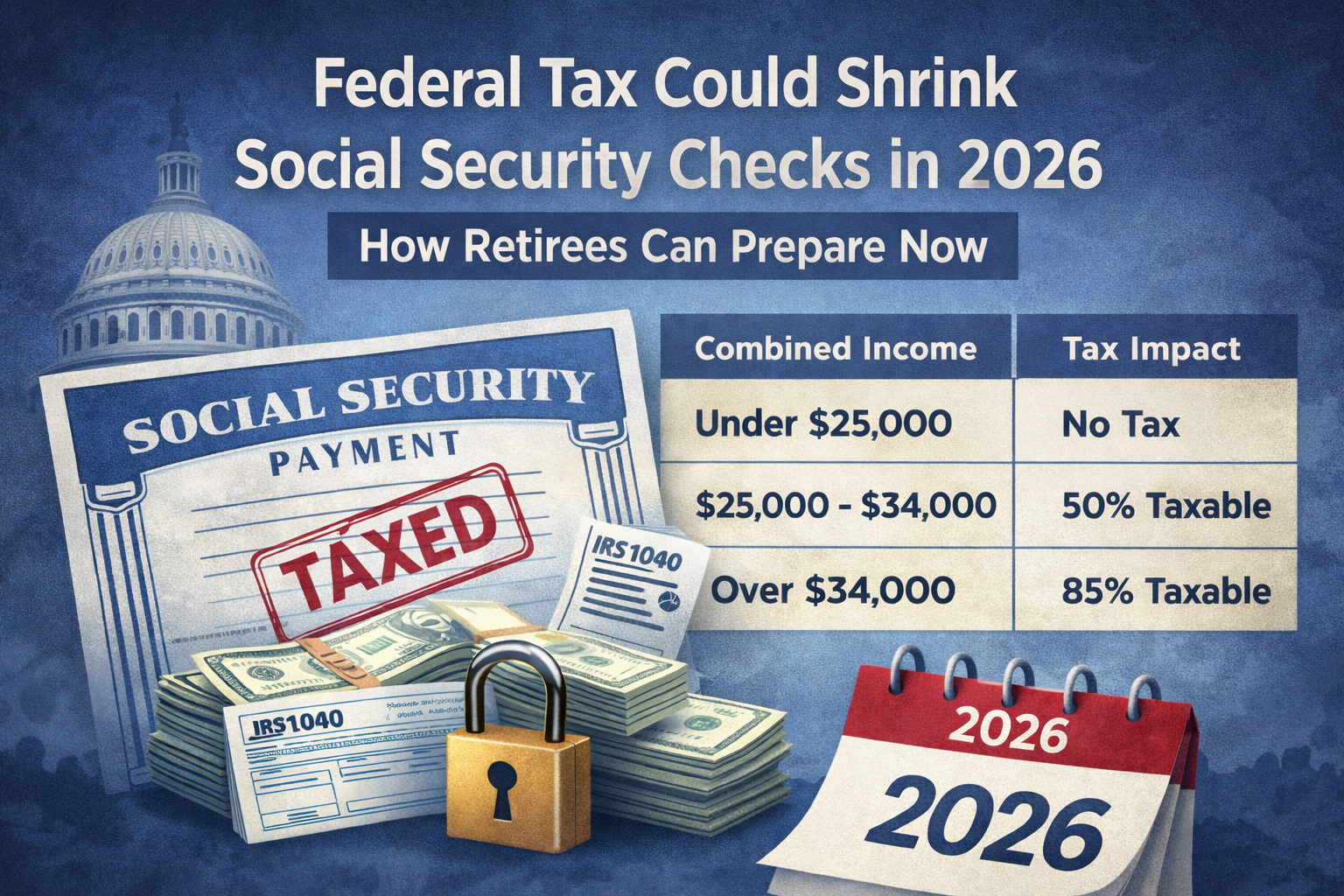

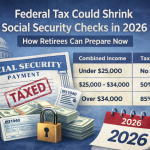

How Social Security Taxes Work

| Combined Income (2026) | Tax Impact on Benefits |

|---|---|

| Below $25,000 (single) / $32,000 (married) | No federal tax on benefits |

| $25,000–$34,000 (single) / $32,000–$44,000 (married) | Up to 50% of benefits taxable |

| Above $34,000 (single) / $44,000 (married) | Up to 85% of benefits taxable |

Important:

This does not mean you lose 85% of your benefit. It means up to 85% of it becomes taxable income, which is then taxed at your normal tax rate.

Who Is Most Likely to Be Affected

You may see smaller net checks if you:

- Have pension income

- Take required minimum distributions (RMDs)

- Work part-time while collecting benefits

- Earn interest, dividends, or rental income

- File jointly with a working spouse

Retirees who rely only on Social Security typically do not pay federal tax on their benefits.

Example: How Taxes Can Reduce Your Net Benefit

| Scenario | Monthly Benefit | Taxable Portion | Estimated Net After Tax |

|---|---|---|---|

| Retiree with no other income | $1,800 | $0 | ~$1,800 |

| Retiree with pension income | $1,800 | 50% taxable | ~$1,650–$1,700 |

| Retiree with IRA withdrawals | $1,800 | 85% taxable | ~$1,500–$1,650 |

(Estimates vary based on tax bracket and state taxes.)

Other Policy Changes Affecting Benefits

Recent legislation repealed older rules that had reduced benefits for some public workers, which increased payments for certain retirees. However, higher benefits can also increase taxable income, potentially offsetting part of the gain through taxes.

In addition, Social Security income taxation applies to retirement, survivor, and disability benefits, not just retirement payments.

Practical Steps to Reduce the Tax Impact

1. Manage Withdrawals Strategically

Consider spreading IRA or 401(k) withdrawals across multiple years to avoid crossing tax thresholds.

2. Use Roth Accounts

Roth withdrawals generally do not count toward combined income, which may help keep benefits tax-free.

3. Time Your Retirement Income

Delaying Social Security or adjusting when you take other income can reduce tax exposure.

4. Consider Tax Withholding

You can request voluntary tax withholding from Social Security payments to avoid a large tax bill at filing time.

5. Review Filing Status

Married couples may benefit from coordinated withdrawal planning to stay below thresholds.

Common Questions

Will everyone pay taxes on Social Security in 2026?

No. Many lower-income retirees will continue to receive benefits tax-free.

Does the tax reduce my official benefit amount?

No. It reduces the net amount you receive after taxes, not the gross benefit.

Are SSDI benefits also taxable?

Yes, SSDI can be taxed under the same income rules.

Do states tax Social Security?

Most states do not, but a few have their own rules.

Key Takeaways

- Social Security benefits may be partially taxable depending on total income.

- A 2026 COLA increase can push more retirees into taxable ranges.

- The tax does not cut benefits directly but reduces take-home income.

- Careful withdrawal and tax planning can minimize the impact.

Planning Ahead for 2026

Retirees should review:

- Total projected income

- Retirement account withdrawal strategy

- Filing status and spousal income

- Potential Roth conversions (if appropriate)

A yearly tax projection can help ensure your Social Security income remains as efficient as possible.

Leave a Comment